FIRM 2.0

Digital map updates accelerating across coastal counties

Risk Rating 2.0

Premiums are property-specific (not just zone letters)

Private Flood

More carriers quoting mitigated homes competitively

Seller Certainty

“Full packet” listings typically close faster

FIRM 2.0

Digital map updates accelerating across coastal counties

Risk Rating 2.0

Premiums are property-specific (not just zone letters)

Private Flood

More carriers quoting mitigated homes competitively

Seller Certainty

“Full packet” listings typically close faster

Coastal Flood Map Updates 2025 (FIRM 2.0): What Changed, Risk Scores, and How to Sell Anyway

A data-journalism guide to FEMA’s modernized flood mapping and Risk Rating 2.0—how new flood zones, elevation rules, and premiums affect owners, buyers, and sellers in 2025. We’ll show you how to price, package, and still sell a coastal home with confidence.

Justin Erickson · CEO, Local Home Buyers USA · Updated

About the author: Justin Erickson leads Local Home Buyers USA, a nationwide team that purchases coastal properties “as-is,” coordinates title/escrow, and helps sellers navigate insurance, municipal, and environmental constraints—including flood-zone reclassifications. Our approach combines certainty (clean timelines, safe closings) with transparency (apples-to-apples net math, multiple exit structures).

Important: This guide is educational and not legal/insurance advice. For coverage and underwriting questions, consult a licensed insurance agent and your lender or attorney.

Key Takeaways

Risk Rating 2.0 (RR2.0) shifted NFIP pricing toward property-specific risk (elevation, distance to water, flood type, replacement cost), not just the zone letter.

FIRMs still matter for compliance and lending. Your map governs required coverage, building standards, and disclosure—even when premiums are individualized.

Elevation Certificates (ECs) aren’t required for RR2.0 quotes, but they can validate lower risk (and reduce buyer anxiety) when your finished floor is above expected flood levels.

Best seller move in 2025: reduce uncertainty. Provide a clean “seller packet” with maps, quotes, mitigation proof, and a closing plan. Certainty is currency.

If you want a faster sale: model three lanes—Cash vs. Novation vs. Retail—so you choose the best risk-adjusted net, not just the highest sticker price.

Context: FIRMs vs. Risk Rating 2.0—what’s actually new in 2025

Flood Insurance Rate Maps (FIRMs) are FEMA’s regulatory maps showing Special Flood Hazard Areas (SFHAs) and Base Flood Elevations (BFEs). Communities adopt them for building codes, elevation requirements, and disclosure. For decades, NFIP premiums largely tracked those zones.

Risk Rating 2.0 modernized NFIP pricing by incorporating additional variables: distance to coast/river, elevation relative to water, flood frequency/severity, and property characteristics (foundation type, first-floor height, replacement cost). In plain English: two homes can share a zone but carry very different premiums.

Seller reality check: You’re not “selling a flood zone.” You’re selling a known risk profile with a clean path to insurance and closing. That’s why the packet matters.

The coastal market rewards sellers who do one thing better than everyone else: remove uncertainty before a buyer has to ask.

Fast definitions (buyer-friendly)

Map risk is your regulatory category (SFHA vs. not). Premium risk is what it costs to insure your exact structure given elevation, distance, and replacement cost. Buyers often confuse the two—your job is to separate them with documents.

Because buyers compare neighbors. Under RR2.0, premiums can diverge due to structural details (first-floor height, foundation type) and property-level risk factors (distance to water, wave energy). A solid seller packet turns “random” into “explainable.”

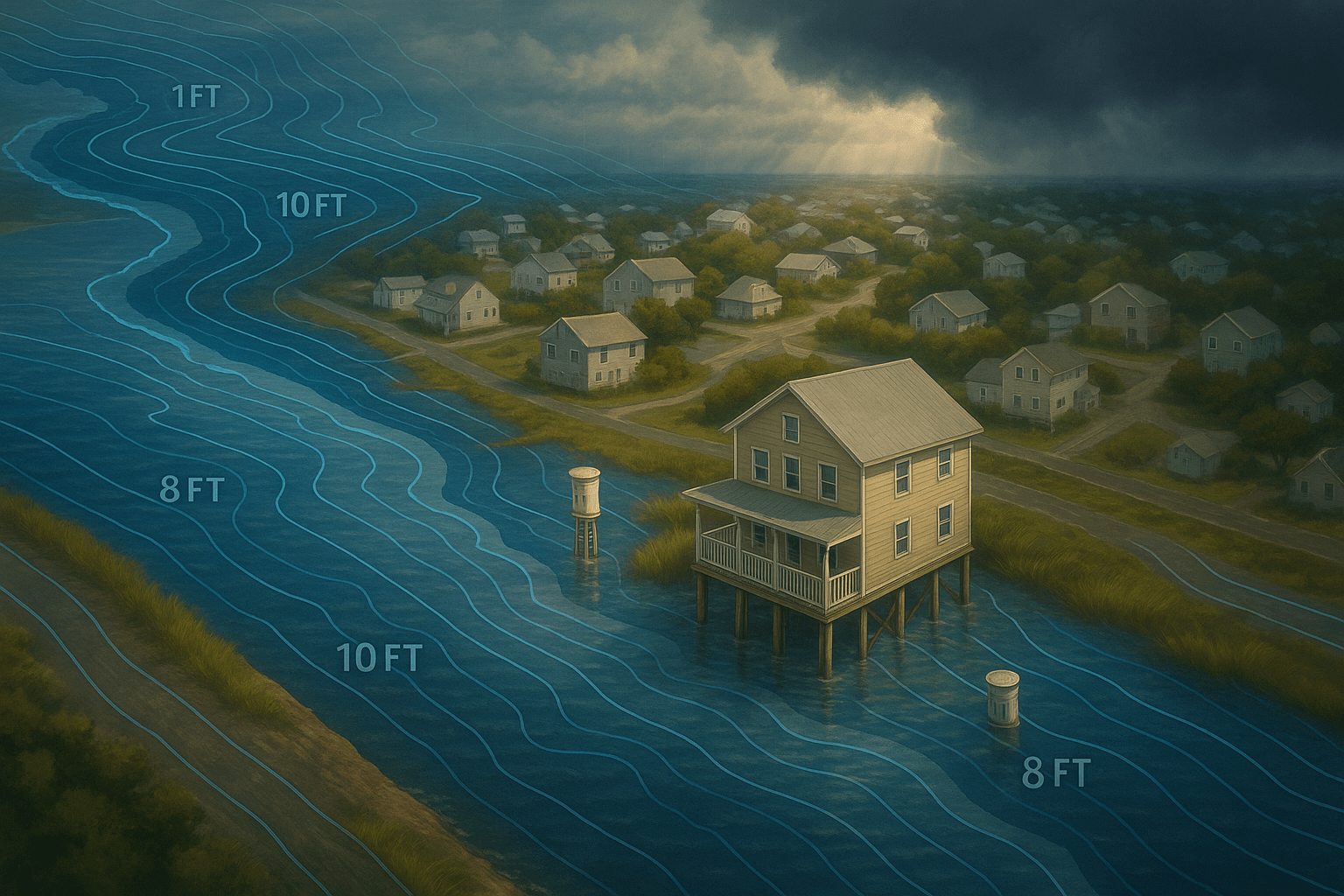

Zones & jargon: AE, VE, AO, X—what they signal to buyers

Zone VE: High-energy coastal wave action. Elevated construction and open foundations (e.g., piles) are common. Buyers expect stricter build standards and a bigger insurance conversation—but well-designed homes still sell fast.

Zone AE: Stillwater flood elevations defined; BFEs shown. Elevation, flood openings, and mechanical placement matter.

Zone AO/AH: Shallow flooding or ponding/overland flow with depths indicated (e.g., “1–3 ft”). Drainage and grading can materially change buyer confidence.

Zone X (shaded/unshaded): Lower probability flood hazard. Not zero risk. Serious buyers still ask: “What’s the insurance cost?” and “What’s the loss history?”

Some communities add LiMWA (Limit of Moderate Wave Action) lines inside AE—areas with 1.5–3 ft breaking waves. For many buyers, LiMWA triggers “VE-style” scrutiny even if the zone letter is AE.

Local nuance: If your map is “preliminary,” lenders may still use effective FIRMs until adoption—while buyers price the risk immediately. Disclose both and label the status clearly.

Premium math: how RR2.0 prices risk (without the alphabet soup)

Think of pricing as a function of exposure and consequence:

Exposure: distance to water, elevation vs. water surface, wave action, frequency, depth grids, local hydraulics.

Consequence: replacement cost, foundation type, first-floor height, and whether utilities/mechanicals sit above expected flood levels.

Elevation Certificates (ECs) are not mandatory for RR2.0, but they’re still powerful. If your home is elevated above BFE (or has compliant flood openings and elevated systems), an EC can document the facts and reduce buyer anxiety—and sometimes improve quotes.

Private flood insurance has expanded. Some carriers price competitively for well-mitigated homes. When selling, collect both NFIP and private quotes with matching coverage/deductibles so buyers can compare apples-to-apples.

Buyers don’t fear water as much as they fear surprise. If you eliminate surprise, you raise offers.

ZIP-In Coastal Exit Console (Illustrative Only)

This console is designed for intuition, not precision. It helps you model two things at once: a simple risk/confidence snapshot and how three exit lanes—Cash, Novation Partner Sale, and Typical Retail Listing—can stack up on net dollars after time and friction.

Step 1 — Risk & Insurance Profile

Offset: +1 ft

Level: Medium

Used for rough premium banding only.

Step 2 — Exit & Net-Proceeds Assumptions

Mortgage + taxes + insurance + HOA.

Defaults: Cash discount ~18%, novation share and days tuned for “partner sale,” and retail assumes 5.5% listing commission plus 1.5% closing costs. Adjust the numbers to feel the spread.

Reminder: This is illustrative. Your actual quotes and net proceeds depend on the property, title, market, and buyer financing.

Step 3 — Modeled Outlook (Not a Quote)

Illustrative NFIP Monthly Band

$180 – $260

Actual quotes depend on underwriting assumptions and more granular data.

Balanced CoastalBalanced risk; documentation matters but doesn’t scare off the right buyers.

This quick label blends zone, elevation, and mitigation into buyer language.

Illustrative Net to You (After Costs & Time)

Cash (as-is, we eat repairs)

$—

Fast lane: we target 7–14 days with clear title, minimal visits, and we handle cleanup.

Partner Sale (Novation)

$—

We upgrade/market; you keep ownership until closing. Built for demand-heavy areas with insurance friction.

Typical Agent Listing (Benchmark)

$—

Repairs, showings, insurance questions, and a longer clock. Commission + closing costs reduce your take-home.

Based on your inputs, we’ll highlight the lane likely to deliver the strongest risk-adjusted net—not just the highest sticker price.

Coastal Seller Packet Builder (Next Level)

If you only do one thing from this guide, do this: build a one-page, buyer-ready packet that answers the questions buyers and lenders ask before they ask them. That’s how you reduce renegotiations, reduce fall-through, and raise the number of serious offers.

Packet Checklist (tap to save)

FEMA Map panel (MSC)

Include effective + preliminary (if available). Highlight your structure, not just the neighborhood.

BFE / finished floor note

A simple statement: “Finished floor is approximately ___ ft above/below BFE.” (Use EC when possible.)

Elevation Certificate (if available)

Not required for RR2.0, but powerful for buyer confidence and quote accuracy.

Mitigation proof

Photos of flood vents/openings, foundation type, elevated mechanicals, and any flood-resistant materials.

Insurance quotes (NFIP + private)

Match coverage/deductibles. Buyers trust side-by-side comparisons.

Loss / claim transparency

If you have claims, summarize the event + repairs + receipts. If none, state “no known flood claims.”

Nearest NOAA gauge link

One link + one sentence: “Nearest station: ____; used for tide/surge reference.”

Title fast-start

HOA contact, payoff lender info, and any known liens or probate context.

Access plan

How showings/inspections will work + safety notes (crawlspace, utilities, tide timing).

Closing plan

Target timeline, preferred title company (if any), and wire verification steps.

Pro move: Put the packet in one PDF and attach it to the listing (or share via link). The first buyer question becomes: “When can we see it?” instead of “What’s the insurance situation?”

When buyers can’t estimate premium, they price the worst case.

Your advantage

Clarity + timeline

Coastal deals reward sellers who can close cleanly.

Paste-ready “buyer email” (preview)

“Hi — attached is our Coastal Seller Packet: FEMA map panel (effective & preliminary), elevation/mitigation details, and insurance quote options (NFIP + private). We’re ready for a clean close and can accommodate inspections quickly. Let us know your preferred closing date and any lender/insurance requirements so we can coordinate.”

Datasets: where to get authoritative maps, tide gauges & risk tools

Use these sources in your disclosure packet and listing documents. They’re stable, official, and updated:

FEMA Map Service Center (MSC) — download effective and preliminary FIRMs, floodways, BFEs, and Letters of Map Change (LOMR).

Packaging tip: Include the MSC panel for your parcel, the EC (if available), and a one-page “Mitigation Fact Sheet.” Add your nearest NOAA gauge link. You’re selling clarity.

Mitigation that moves the needle (and documentation buyers trust)

Flood-damage-resistant materials below expected flood levels; sealed penetrations where appropriate.

Drainage & Access

Lot grading and swales; check culvert capacity and maintenance responsibility.

Document pump stations, tide gates, berms, or community mitigation projects (if applicable).

Proof of maintenance: roof/gutter logs, vent clearances, service tags with dates.

Aerial context matters: contours + tide markers give buyers an anchor for rational pricing.

Insurance effect: Mitigation documentation can improve both NFIP and private quotes. Even when premiums remain high, buyers accept costs more readily when they see the home is engineered correctly and the expected inundation depth at finished floor is low for common events.

Pricing & offer strategy: cash vs. retail vs. novation on the coast

Coastal deals reward certainty. If your home is well-elevated and documented, retail buyers may pay near-market. If elevation is marginal—or insurance is heavy—cash buyers may win once you model timeline risk, inspection drift, appraisal/insurance friction, and carrying costs.

Quick Compare

Cash (as-is): Shortest path, minimal visits; often 7–14 days with clear title; discount reflects risk + carry cost avoided.

Retail: Requires a strong packet (EC/mitigation/quotes), clean access, and insurance clarity for lender. Longer clock, potentially higher net.

Novation: We upgrade/market while you retain ownership until closing; net can exceed cash when demand exists and insurance concerns are solvable.

We buy coastal homes “as-is,” with clear timelines and safe closings. Get an apples-to-apples comparison of Cash vs. Novation vs. Retail—including insurance scenarios and net math for your specific ZIP.

Local title partners · Insurance coordination · 7–30 day closings · Transparent reports you can share with family or advisors.

Flood-zone deals live or die in the paperwork. Start title day one, lock insurance conversations early, and coordinate municipal items before the final walkthrough.

Title & payoffs: open immediately; collect HOA estoppels and municipal utility balances.

Final utility reads & possession photos at transfer

Pricing & Narrative

Explain RR2.0 briefly; show why mitigation lowers exposure

Provide cash and retail paths with realistic timelines

Offer to transfer mitigation know-how (vendor list, maintenance logs)

Want us to price your coastal exit (in writing)?

We’ll run your property through a simple, seller-friendly decision sheet: Cash vs. Novation vs. Retail, with timeline assumptions, insurance friction notes, and net math you can share with family or advisors.

Fastest path: start your seller packet above, then request your offer.

Do I need an Elevation Certificate to sell or to get NFIP insurance?

No—RR2.0 doesn’t require an EC. But an EC can document higher first-floor elevations, compliant openings, and other features that may reduce quotes and calm buyers. If your house is elevated, an EC often pays for itself in confidence.

If my preliminary map shows a new SFHA, can I still sell before adoption?

Yes. Effective FIRMs generally govern lending until your community adopts the new maps. But buyers will price the preliminary information. Disclose both and label the status clearly in your seller packet.

Will premiums always rise under RR2.0?

Not always. Some policies decrease; others step up over time. Mitigation and alternative private quotes matter. The best seller move is to provide side-by-side quotes so buyers can plan.

Can you buy my coastal home “as-is” with a fast close?

Yes. We purchase “as-is,” coordinate title and insurance details, and can close in as little as 7–14 days with clear title. We’ll show cash vs. novation side-by-side so you choose the best net.

RCI · Certainty Discount now visible as a line-item in every offer.

BDI · Buyer Demand Index translates absorption into timeline guidance.

FOS · Friction-to-Offer Score surfaces readiness tasks in your portal.

LESI · Local Economic Stability Index monitors macro-local shocks.

Anxiety Premium Index tracks hyperlocal sentiment beyond AVMs.

RCI · Certainty Discount now visible as a line-item in every offer.

BDI · Buyer Demand Index translates absorption into timeline guidance.

FOS · Friction-to-Offer Score surfaces readiness tasks in your portal.

LESI · Local Economic Stability Index monitors macro-local shocks.

Anxiety Premium Index tracks hyperlocal sentiment beyond AVMs.

Research Hub — Indices, Methods & Transparency

Explore the indices and pricing rails powering Local Home Buyers USA. We don’t guess. We model —

then expose the math for sellers, partners, and regulators.

PricingMethod

Unified PropTechUSA.ai Net Offer Sheet

How our indices come together into a single, seller-facing offer with transparent line-items and guardrails.