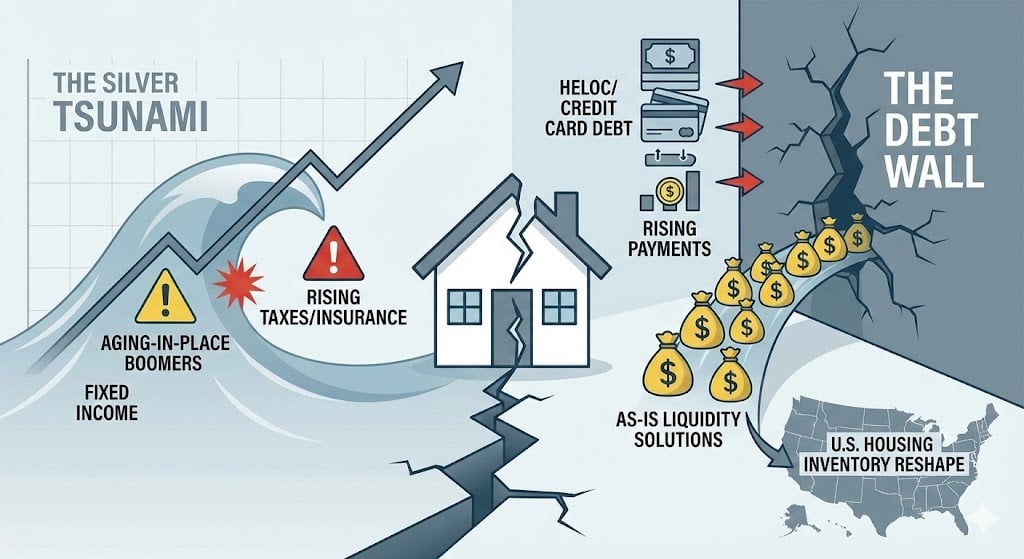

For most of the last decade, the phrase “Silver Tsunami” has been used like a storm warning: tens of millions of Baby Boomers, many aging in place, eventually listing and selling their homes. At the same time, a quieter, sharper risk has emerged: the Debt Wall — a combination of higher payments, rising taxes and insurance, and consumer debt that chips away at fixed incomes.

At Local Home Buyers USA, backed by the research engine of PropTechUSA.ai , we don’t treat those as two separate stories. We model them together:

Not a wave of desperate foreclosures, but a large, ongoing rotation of equity-rich, cash-poor owners into “as-is” liquidity paths.

This piece is a roadmap for:

- Aging owners weighing whether to stay, sell, or partner.

- Adult children and heirs trying to protect family equity.

- Advisors, attorneys, and planners who need a clearer playbook for the next 5–10 years.

It also connects to our broader research on how capital actually flows through today’s housing system: America’s “As-Is” Divide , our probate selling guide , and the national safety net framework outlined in Beyond “We Buy Houses” .

The Boomer Household Budget Squeeze: Equity on Paper, Tension in Cash Flow

When most people hear “Boomer homeowner,” they picture a paid-off house and a comfortable retirement. The reality we see in our intake calls and data feeds is more complicated.

Many older owners are sitting on six- and seven-figure equity positions while juggling:

- Property taxes that have quietly doubled or tripled in 10–15 years.

- Homeowners insurance premiums re-rated for storms, wildfires, or crime risk.

- HELOC balances from previous remodels or debt consolidations.

- Credit card and medical debt on top of fixed Social Security and pension income.

Add in maintenance: roofs, HVAC, foundations, siding, driveways, and accessibility retrofits (ramps, bathrooms, railings) that were never budgeted for.

We see the same pattern when we model “as-is” risk in our PropTech 2.0 evolution research : macro narratives matter, but household-level cash flow is where decisions are actually made.

Where the Debt Wall Actually Shows Up

Our internal analytics stack, the same engine we use for “as-is” capital mapping , tracks several telltale signs that a household is drifting toward a decision point:

- Tax delinquency and code enforcement trends in historically “stable” neighborhoods.

- Insurance non-renewals and premium spikes following regional weather events.

- Refinance and HELOC data from prior low-rate eras rolling into higher-rate resets.

- Inbound lead language that has shifted from “curious about selling” to “I can’t keep up.”

None of these guarantee a sale. But taken together, they form the contours of the Debt Wall: a line where continuing to carry the home, as-is, becomes mathematically and emotionally unsustainable.

Silver Tsunami Stress Lab™ — Model Your Cash-Flow Pressure in 60 Seconds

Use this quick, anonymous sandbox to see how your monthly budget lines up with the Debt Wall. It’s not financial advice or an offer—just the same cash-flow lens our team uses when we talk with aging owners, adult children, and advisors across all 50 states.

1. Your Quick Snapshot

2. Your Debt Wall Snapshot

Cash-Flow Pressure Index

We’ll show how much of your monthly income is being eaten by housing + debt.

Debt Wall Proximity

We’ll translate those numbers into “how close” you are to needing a decision.

Suggested Liquidity Lens

See whether you’re in “plan early,” “plan now,” or “time to act” territory—and how an as-is option might fit into the mix.

This lab is for education only and does not create a client relationship or guarantee any outcome. Real decisions should be made with full financial, legal, and tax advice. When you’re ready for a human second opinion, you can start a conversation here.

How the Silver Tsunami + Debt Wall Actually Reshapes Inventory

It’s tempting to imagine a single moment when millions of listings flood the MLS. That’s not how this works. In practice, the Silver Tsunami plus the Debt Wall produces a rolling, uneven wave of as-is opportunities, clustered by:

- Tax and insurance regimes (state and county level).

- Local economic shocks (plant closures, rate-sensitive industries, healthcare hubs).

- House age and deferred maintenance pockets.

In our research on America’s “As-Is” Divide , we showed how investor capital clusters tightly in certain “easy-to-underwrite” ZIP codes while bypassing more complex, older, or lower-price neighborhoods. The Silver Tsunami + Debt Wall dynamic amplifies that divide:

ZIP Codes That Attract Capital

- Moderate price bands that support clean yield math for investors.

- Comparables that make condition-adjusted pricing straightforward.

- Stable or improving school + crime scores.

- Predictable holding costs and insurance profiles.

In these areas, aging owners under pressure have multiple options: list, sell as-is, or partner with a professional buyer on a more creative structure.

“As-Is Deserts” That Stay Stuck

- Very low price bands where rehab budgets don’t pencil.

- High perceived risk: code issues, environmental concerns, or weak rental demand.

- Fragmented housing stock with a history of investor burn-out.

In these deserts, aging owners may be equity rich on paper but effectively trapped: traditional buyers shy away, and standard “we buy houses” marketing never materializes into reliable offers.

Closing that gap is a core part of PropTechUSA.ai’s mission, and a big reason we built the nationwide safety net model described in Beyond “We Buy Houses” .

As-Is Liquidity as a Safety Net — Not a Last Resort

Older owners and their families are often told: “Just list it. Let the market decide.” That advice assumes:

- The home is easily financeable in its current condition.

- The seller can navigate showings, inspections, and repair negotiations.

- There’s enough runway to ride out a long days-on-market stretch.

For many Silver Tsunami + Debt Wall households, none of those assumptions hold. What they actually need is structured, transparent as-is liquidity that:

- Respects the real equity they’ve built.

- Acknowledges the cash-flow pressure they’re under.

- Protects their dignity, privacy, and timeline.

How PropTechUSA.ai Underwrites Silver Tsunami + Debt Wall Risk

At the research layer, we bring the same discipline we use in our probate compression modeling and 2030 closing stack roadmap :

- Tax and insurance trajectories at the county and ZIP level.

- Age-of-stock + condition proxies to estimate near-term repair cliffs.

- Consumer debt and delinquency signals that precede listing or distress.

- Investor appetite by price band and rehab budget tolerance.

The outcome isn’t a single algorithmic “take it or leave it” offer. Instead, it’s a menu of realistic paths that a family can weigh with eyes open.

2025–2030: What We Expect to See as the Silver Tsunami Meets the Debt Wall

We don’t claim to know the exact rate path or every policy response that will shape the next five years. But when we stress-test our models, a few themes repeat:

-

Gradual but persistent increase in “needs work” listings.

More older-owner homes will hit the market with visible deferred maintenance, especially in markets where insurance and taxes spike. -

Uneven bargaining power.

In some ZIPs, demand will still outstrip supply, even for dated homes. In others, condition issues plus payment pressure will force sellers to accept steep discounts or face long marketing times. -

More heirs opting for as-is sales over “one more renovation.”

Adult children will increasingly choose to preserve time and sanity over squeezing out every last dollar with renovations, especially when they live out of state. -

Nationwide buyers with real underwriting winning share.

Sellers will gravitate toward operators who can show their math and close reliably, not just throw out a postcard slogan.

That last point is a big part of why we built Local Home Buyers USA the way we did: 50-state coverage, structured as-is offers, and a research layer that treats aging owners as first-class decision-makers, not an afterthought.

Want a Clear Picture Before the Pressure Builds?

Whether you’re an aging owner, a family member, or an advisor, the most powerful move you can make is simple: see all your options on one page before the Debt Wall forces a rushed decision.

Our team will walk your property through the same research lens we apply in our nationwide safety net work — and give you a calm, as-is set of scenarios to compare.

FAQs: Silver Tsunami, Debt Wall & As-Is Selling

Do I have to be “desperate” to consider an as-is sale?

No. In our world, as-is does not mean distressed. It simply means the property is being valued and purchased with real-world condition and risk factored in. Many of the families we help are quietly equity-rich and just want a clean, dignified transition without dragging the process out over months.

How do you protect older sellers from being taken advantage of?

First, we show our math in plain English: how we think about repairs, timelines, and resale risk. Second, we encourage involving trusted family members or advisors in the conversation. Third, we build our process around documented offers, reputable title/escrow or attorneys, and clear closing timelines. Our safety net model is designed for transparency and consent, not pressure.

Can we sell a parent’s home even if we’re still in probate?

In many cases, yes—with the right structures and court approvals. That’s exactly why we created our dedicated guide on buying homes in probate . The key is aligning legal authority with realistic timelines so equity doesn’t quietly erode while everyone waits.

What if taxes and insurance keep rising after we sell?

That’s precisely why we emphasize timing. If you already suspect your current payments are unsustainable, it usually doesn’t get “easier” three years from now. Our job isn’t to scare you—it’s to help you map what happens to net proceeds under different timing scenarios so you can decide, eyes open, if now, later, or “not yet” makes the most sense.

How does this connect to your broader proptech work?

The Silver Tsunami + Debt Wall is one of the core scenarios we model in our PropTechUSA.ai research program . It’s the same lens we use to study as-is deserts, probate compression, and our 2030 digitized closing stack . The through-line is simple: a more honest, more protective system for sellers the traditional market wasn’t built to serve.