PropTechUSA.ai Research • Local Home Buyers USA

The 2030 Home Sale: A Day-in-the-Life of a Seller in a Fully Digitized Closing Stack

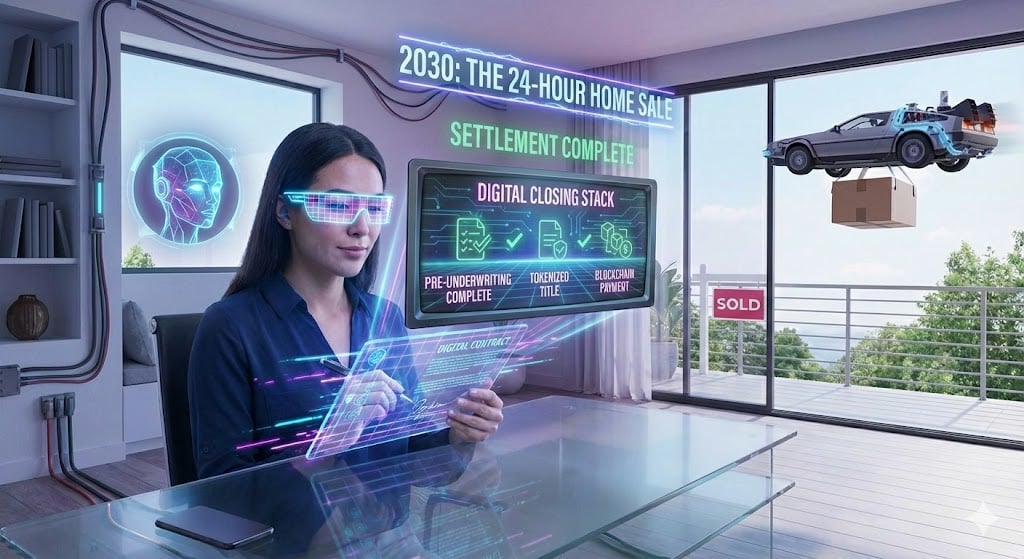

It’s 2030. Title is tokenized, underwriting is continuous, clear-to-close is measured in hours, and settlement happens on-chain while you’re at lunch. This is a narrative walkthrough of a single seller’s day inside a fully digitized closing stack — and how what we’re building at Local Home Buyers USA, powered by PropTechUSA.ai, is the first step toward that future.

TL;DR — A 24-Hour, Fully Digitized Home Sale

- Instant pre-underwriting: your “sellability file” is continuously updated in the background, not assembled in a panic.

- Tokenized title: ownership lives as a programmable token, simplifying liens, permissions, and transfer.

- 24-hour clear-to-close: KYC, LTV, and compliance are pre-cleared; the “closing” is a confirmation, not a gauntlet.

- Blockchain settlement: funds and title move together in an atomic transaction — no dangling wires or “did it fund?” calls.

- Today’s bridge: our sentiment models, liquidity indexes, and Compare Home Offers engine are v1 of that 2030 experience.

Want to see the 2030 mindset applied to 2025 reality? Get a net-first offer →

Imagine you wake up tomorrow and selling your house feels more like closing a high-limit credit card account than orchestrating a small corporate merger. No stacks of paper. No 45-day maybe-it-closes, maybe-it-doesn’t suspense. Just a clear interface, a few high-stakes decisions, and a 24-hour, end-to-end settlement.

That’s the 2030 home sale this piece explores — not as sci-fi, but as a structured “day in the life” based on technology that already exists in fragments today: real-time risk models, tokenized ownership, instant identity verification, and programmable money.

At Local Home Buyers USA, our research arm PropTechUSA.ai is building the bridge from 2025 reality to that 2030 stack. Our work on HSS/API home-sale sentiment , the Seller Stress & Liquidity Index , and algorithmic valuation blind spots is version 0.9 of that future.

Note: This narrative is a forward-looking scenario, not a product announcement or legal promise. It’s meant to help sellers, operators, and investors think concretely about where closing infrastructure is heading — and how to prepare now.

Interactive: 2030 Closing Stack Console

Use this console to see how different closing rails — paper-heavy 2020 stacks, 2025 hybrid workflows, and 2030-digitized infrastructure — change time-to-done, friction, and settlement confidence. It’s a visual model, not legal or underwriting advice, but it mirrors how we think about net, time, and risk inside Local Home Buyers USA and PropTechUSA.ai.

Choose the rails you’re effectively on today — or the rails you want to be on.

The core stack is the same, but what “good” looks like changes slightly by seat.

Typical · a few wrinkles

This is a mental model for 2030-style closing stacks, not a quote, guarantee, or live underwriting engine.

- Identity & KYC Login vs. paper ID

- Title & Liens Token vs. PDF chain

- Underwriting & Risk Continuous vs. one-time

- Funding & Escrow Digital vault vs. siloed wires

- Settlement & Recordation Atomic vs. manual stitching

7:32 a.m. — The Morning Ping: “You’re Clear to List Today.”

Our 2030 seller — call her Maya — doesn’t start her day by googling “what is my house worth.” She wakes up to a notification from her home stack app:

“Liquidity Window: Favorable — Buyer demand for 3-bed homes in your micro-market is in the top 20%. Estimated time-to-offer: 3.2 days. Estimated time-to-close with instant buyer: 24 hours.”

Behind that one sentence is a live mesh of data: sentiment models like our HSS/API framework , mortgage spread signals similar to our 10Y vs 30Y fixed monitoring , and a seller stress profile akin to our Liquidity Index .

The app already knows:

- Maya’s equity and mortgage balance (via secure lender APIs).

- Her rough relocation window (synced from a job-offer document she agreed to share).

- Her home’s condition tier, updated from periodic photo scans and IoT signals.

Instead of a cold “what’s my value?” search, she’s stepping into a pre-underwritten context: the system tells her this is a good week to move, and approximately what “done” could look like if she taps sell.

8:15 a.m. — Tokenized Title, Real-World House

When Maya taps “Explore my exit options”, she’s not just filling in a form; she’s authorizing a set of smart permissions around a tokenized title record.

In 2030, her ownership is represented by a governed token in a permissioned ledger maintained by a consortium of title companies, regulators, and clearing banks. That token carries:

- Her verified identity and co-owners.

- Open liens, easements, and HOA covenants.

- Prior insurance and claim data.

- Rules about who can see what, and when.

Instead of a frantic “title search” weeks into escrow, her title status is continuously reconciled. When she hits “Share with marketplace,” she’s not uploading PDFs; she’s granting query rights to specific buyers and underwriting agents.

This removes one of the biggest wild cards in today’s deals: discovering late in escrow that something in the chain of title or payoff stack doesn’t match reality. In Maya’s world, those mismatches get flagged years earlier — or are corrected in near real time.

9:45 a.m. — Instant Pre-Underwriting & the Offer Board

By mid-morning, Maya has completed exactly three simple confirmations:

- “Yes, I still plan to move by this date range.”

- “Yes, these photos still reflect my home’s interior.”

- “Yes, you can share my pre-underwritten profile with verified buyers.”

On the other side, buyers aren’t guessing. Their underwriting rails pull:

- Real-time sentiment and demand scores (HSS/API-style signals).

- Micro-location risk and insurance inputs (flood, fire, premium shocks).

- Liquidity metrics that echo our liquidity index research .

Within minutes, an Offer Board populates in her app:

- Instant Cash (24-hour close): Net-to-you range with fees and taxes calculated upfront.

- Partnered Upgrade (novation-style): Operator fronts improvements, shares upside — expressed in clear percentages and ranges.

- Retail-First Listing: A predictive DOM window built on models like our Sentiment & DOM analysis .

Each tile shows:

- Expected net in today’s dollars.

- Time-to-done (not just time-to-contract).

- Risk bands: how often comparable deals fall out or re-trade.

This is the 2030 cousin of what we already do with our public Compare Home Offers framework and internal net-offer sheets. The packaging is sleeker; the principle is the same: compare paths on net, time, and risk — not just sticker price.

2:10 p.m. — Smart-Contract Signing & 24-Hour Clear-to-Close

After a midday coffee and a call with her advisor, Maya chooses the Instant Cash tile. She doesn’t download a 35-page PDF; she opens a deal capsule:

- Plain-language summary (inspired by today’s net-offer sheets).

- Smart-contract terms (encoded in a standardized language regulators and counterparties can parse).

- Branching rules (what happens if closing date moves, if a payoff is higher, if a lien appears).

Identity is confirmed with a single biometric tap backed by multi-factor checks across her bank, government ID, and prior verified transactions. On the buyer side, funding is pre-locked in a compliant digital escrow that behaves like a dedicated wallet for this transaction.

The magic phrase for her: “Estimated Clear-to-Close: 24 hours, subject to final automated checks.”

Behind the scenes, the closing stack runs:

- KYC/AML on all parties.

- Automated lien and judgment sweeps.

- Insurance binder confirmation.

- Automated “know your property” rules built on decades of legacy title policy data.

In 2025, we approximate this through fast title partners, digital signatures, and tight internal checklists. In 2030, the system itself becomes an always-on underwriter that treats a single home sale like a small but fully-digitized capital markets event.

7:26 p.m. — Atomic Blockchain Settlement While Dinner’s in the Oven

The next evening, a final notification slides across Maya’s screen:

“Settlement window opened. Review final net and confirm transfer.”

One last summary shows:

- Final sale price.

- Payoffs, taxes, and fees.

- Exact net to her primary bank and optional distribution to a second account or investment wallet.

When she taps “Confirm settlement”, a single atomic transaction executes:

- The title token moves from Maya’s identity to the buyer’s.

- Funds flow from the buyer’s escrow vault to:

- Her payoff lender(s).

- Tax authorities.

- Her personal accounts.

- The operator’s fee account.

- The ledger updates escrow and title databases simultaneously.

There is no “wire sent, did it land?” anxiety. No waiting on a Friday 4:57 p.m. confirmation. The chain either records a completed atomic settlement — or it doesn’t execute at all.

For Maya, the impact is simple: she knows, in near-real time, that she is no longer the owner, her mortgage is paid, and her proceeds are available. For operators and investors, the impact is deeper: a programmable closing stack capable of handling thousands of such micro-events with audit trails built in.

What We’re Already Doing in 2025 to Make This Real

The 2030 stack sounds futuristic, but the building blocks are already here — and we’re using many of them today inside Local Home Buyers USA and PropTechUSA.ai.

-

Continuous sentiment & liquidity modeling

Our HSS/API sentiment and Seller Stress & Liquidity Index research are first-generation versions of the “morning liquidity ping” Maya sees. -

Algorithm reality checks

Our deep dive on Zestimate blind spots is the philosophical core of PropTech 2.0: algorithms are inputs, not verdicts. -

Net-focused offer design

Tools like Compare Home Offers already present multiple paths (cash, hybrid, retail) with transparent math. That’s the early version of Maya’s Offer Board. -

Digital-first workflows

E-sign, fast title partners, and unified net-offer sheets are our 2025-level infrastructure for compressing time-to-close without skipping diligence.

We’re not promising 24-hour atomic settlements everywhere tomorrow. But every dataset we publish, every research piece we ship, and every net-offer we structure is intentionally pointed at that 2030 horizon.

Seller Playbook: How to Prepare for a 2030-Style Sale Today

You don’t need a tokenized title to start thinking like a 2030 seller. Here are practical steps you can take now:

-

Centralize your documents

Keep payoff statements, HOA docs, insurance info, and prior inspection reports in one secure digital folder. The more “pre-underwritten” your file is, the faster a modern operator can move. -

Track net, not just Zillow

Use our Compare Home Offers framework to compare real nets across cash, hybrid, and retail — think like a capital allocator, not just a list-price shopper. -

Watch timing signals

Follow indicators like mortgage spreads and local sentiment — or piggyback on ours via Mortgage Spread Watch and related research. -

Choose partners who show their work

A future-fit buyer or operator will explain how they price risk, time, and fees — not just give you a single “take it or leave it” number. -

Think in exit paths, not one path

Cash, creative structures, and retail listings all have a place. 2030-style infrastructure simply makes switching between them easier; the mindset starts now.

If you want help applying a 2030 lens to a 2025 decision, that’s exactly what Local Home Buyers USA is built for: net-focused, research-driven options, with humans still on the other side of the screen.

Ready to Sell Like It’s 2030 — Using Today’s Tools?

Fully digitized closings, tokenized title, and atomic settlement are coming. You don’t need to wait for the entire ecosystem to catch up to start benefiting from the mindset: price time, understand liquidity, and partner with operators who treat infrastructure as a feature, not an afterthought.

At Local Home Buyers USA, powered by PropTechUSA.ai, we’re already shipping the research and workflows that make a 24-hour, certainty-first closing more likely — even in a very human 2025 market.

FAQs: 2030 Closings, Tokenized Title, and Today’s Reality

Is a 24-hour home sale actually realistic by 2030?

In every market and price band, probably not. In specific, well-regulated rails — highly digitized title jurisdictions, standardized loan products, simple single-family properties — a 24-hour clear-to-close window is plausible. The point isn’t “every sale in a day,” but “far fewer deals dragged out by avoidable friction.”

What does “tokenized title” really mean?

It does not mean a speculative NFT of your house. It means that the legal record of ownership and certain encumbrances are represented as a governed, programmable token on a permissioned ledger. That token can enforce who’s allowed to transfer, inspect, or pledge the asset — and can move in sync with funds during settlement.

How is Local Home Buyers USA moving toward this future now?

We don’t control national title rails, but we do control how we model offers and run our own workflows. That’s why we invest heavily in research like our home-sale sentiment models, seller stress and liquidity work, and algorithm blind-spot analysis — and why we design offers around net, time, and risk instead of only price.

Do I need to understand blockchain to benefit from a digitized closing stack?

No. The goal of good infrastructure is to disappear into the background. In a mature 2030 stack, sellers and buyers interact with simple, human-readable summaries and clear choices; the ledgers, smart contracts, and compliance checks run underneath, the way payment networks do today.