Are “Online Property Companies” Asking You for Money? Read This Before You Get Scammed.

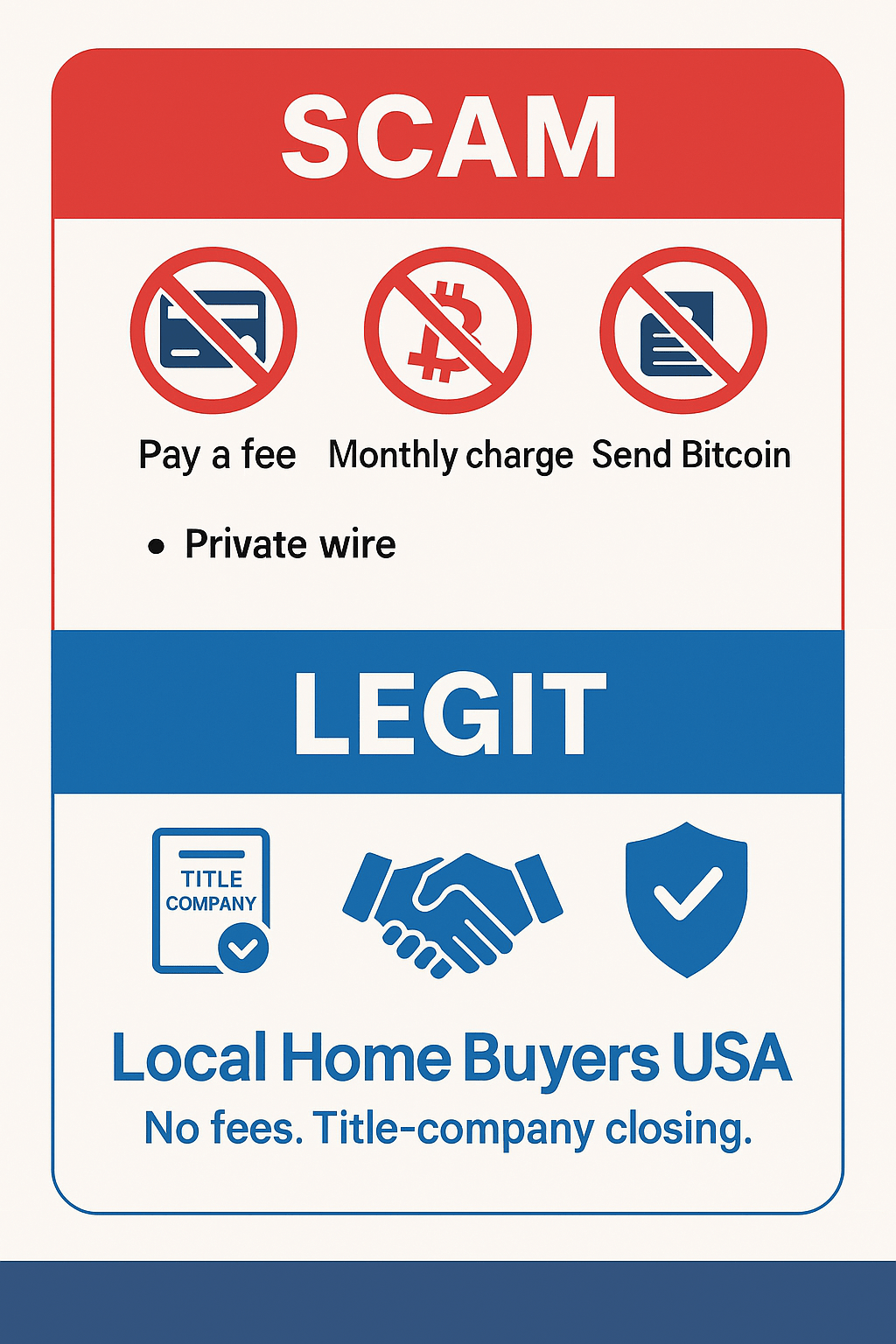

If a “home buyer” or “online property company” asks you to pay a fee, subscribe monthly, send crypto, or wire money to an individual, you’re almost certainly staring at a scam. Legit buyers pay you and close through a licensed title company or closing attorney. At Local Home Buyers USA, we will never ask for your money—ever.

Interactive: Scam Risk Console

Flip the switches that match what a so-called “buyer” is asking you to do. We’ll estimate your scam risk in real time.

- They want an upfront “activation” or “priority” fee from you.

- They ask for crypto / gift cards / P2P app payment.

- They refuse to use a licensed title company or closing attorney.

- They won’t provide proof of funds or a written purchase agreement.

- They want you to wire to a private account instead of title.

Tip: if more than two switches are on, you are almost certainly dealing with a scammer.

You haven’t turned on any red flags yet. A real buyer still shouldn’t ask for your money, but you’re not in obvious danger based on these questions alone.

1) Real Buyers vs. Scam Operators

What Real Buyers Do

- Pay you for your house—no seller fees, no monthly charges.

- Provide a written purchase agreement with plain terms.

- Open escrow and close through a licensed title company or closing attorney.

- Place earnest money with the title/escrow agent (not with an individual).

- Offer appropriate proof of funds for the price and market.

- Disburse your proceeds via verified wire or check from title.

What Scammers Do

- Ask you to pay an “activation,” “marketing,” or “priority” fee.

- Bill your card for a monthly subscription tied to nothing real.

- Request Bitcoin, gift cards, or P2P transfers to “hold” your place.

- Demand a private wire outside of a title company.

- Refuse to show proof of funds or avoid written contracts.

- Pressure you to act immediately or “lose the deal.”

2) The Real-World Numbers (2023–2025)

Scams thrive in uncertainty. These independently reported datasets show how big the fraud problem is across the U.S. The patterns—business email compromise, account takeovers, and wire redirection—mirror the exact plays scammers run against homeowners and title companies.

| Dataset | What It Measures | Year | Key Figures | Source |

|---|---|---|---|---|

| FBI Internet Crime Complaint Center (IC3) – Business Email Compromise (BEC) | Losses from email-based payment diversion scams (often targeting real estate closings) | 2023 | ≈ $2.9B in adjusted losses across ~21,000 BEC complaints | FBI IC3 2023 |

| FTC Consumer Sentinel Network – Fraud Reports | Consumer-reported fraud losses across categories | 2023 | ≈ $10B in reported losses; median loss ~ $500; top contact methods: social media & phone | FTC 2023 |

| FinCEN – Real-Estate Wire Fraud Advisories | Patterns of wires diverted during real-estate transactions | 2022–2024 | Ongoing alerts on spoofed title emails and last-minute wire changes | FinCEN |

| ALTA – American Land Title Association Alerts | Title industry reports on wire-fraud attempts & best practices | 2021–2024 | Escalating attempts to intercept seller proceeds; heavy emphasis on call-back verification | ALTA |

Why these numbers matter for homeowners

- BEC fuels real-estate wire fraud. The same playbook used to hijack corporate wires is used to steal seller proceeds on closing day.

- Crypto & gift card requests are untraceable by design. Reported losses under-count reality because many victims never file.

- Title companies are the choke point for safety. When every dollar routes through licensed escrow, fraud opportunities plummet.

3) The 7 Most Common Tactics (Explained)

- Activation Fee Bait: “Pay $199 to unlock your offer.” After you pay, the rep disappears or keeps upselling tiers that lead nowhere.

- Subscription Trap: A site quietly signs you up for “premium exposure” while delivering no buyers. You notice charges only after months.

- Crypto/Gift Card Hold: A fake “investor” asks for Bitcoin or gift cards to prove you’re serious. Real estate closings do not require this—ever.

- Private Wire Request: Someone sends bank details for a personal account, claiming it’s faster than title. That’s how proceeds vanish.

- Title Company Impersonation: Scammers spoof a title email and send new wire instructions minutes before closing. The phone number in the email is also spoofed.

- Pay-to-Increase Your Offer: “Upgrade to priority for $299 and we’ll raise your price.” Prices are set by numbers, not by fees.

- “Administrative Fee” Drift: Shady operators add junk fees at the end. If a fee exists, it should be disclosed on the title company’s settlement statement long before closing.

4) 15 Red Flags That Usually Mean “Scam”

Immediate Walk-Away Signs

- Any upfront payment to “start,” “activate,” or “secure” an offer.

- Requests for Bitcoin, gift cards, or P2P transfers.

- Directions to wire to a private account—not to a title company.

- Pressure that you must act today to keep your price.

- Refusal to use a licensed title company or closing attorney.

Serious Risk Indicators

- No proof of funds offered—ever.

- Unprofessional emails with obvious misspellings; free email domains.

- No local address; cannot identify a real office or team.

- Refusal to place earnest money into title/escrow.

- “Administrative” or “platform” fees silently added near closing.

Tip: If you spot two or more red flags, freeze the conversation and call a title company yourself using a number you find independently, not from the suspicious email thread.

5) Closing 101: How Legit Deals Actually Work

Step-by-step

- Discovery: You share property basics and your timeline. No payments requested.

- Written Offer: You receive a plain-English purchase agreement with price, earnest money, inspection timeline, and closing date.

- Open Escrow: The buyer deposits earnest money with a licensed title company or closing attorney.

- Title Work: Title searches records, resolves liens, and prepares closing documents.

- Walk-through (as needed): The buyer verifies condition; any adjustments are handled via addenda.

- Final Settlement Statement: You review all numbers well before closing day.

- Closing Day: You sign; title disburses your proceeds by verified wire or check. Done.

Notice what’s missing: credit-card forms, monthly subscriptions, crypto deposits, and private wires. Those belong to scammers—not closings.

6) Exactly How Local Home Buyers USA Protects You

Zero Seller Fees

No “activation,” “admin,” or “marketing” charges—ever. We pay closing costs we agree to, and we never ask you for card details.

Title-First Process

Every dollar flows through a licensed title company or closing attorney in your state. Your proceeds come from title, not an individual.

Proof of Funds

We provide appropriate verification for your market, so you know we can close.

Transparent Agreements

Plain terms, clear contingencies, documented timelines. Questions welcome.

Secure Comms

No last-minute wiring changes by email. We use call-back verification to title.

Nationwide Coverage

We coordinate with reputable title partners across the U.S. for consistent safety.

7) The No-Fee Verification Checklist

Use this before you proceed with any buyer. If the answer is “no” more than once, you’re not ready to move forward.

- Are they asking you to pay anything (now or monthly)? If yes, stop.

- Did you receive a written purchase agreement with clear terms?

- Did the buyer open escrow with a licensed title company/attorney?

- Can the buyer show proof of funds?

- Are wires and checks handled by the title company only?

- Do you understand earnest money (amount, where it’s held, when it’s refundable)?

- Are closing costs and fees disclosed on the settlement statement before you sign?

- Will you receive funds from title on closing day?

8) Word-for-Word Scripts to Shut Down Scammers

“We just need your $199 activation fee.”

You: “Real buyers don’t charge sellers to start a file. I won’t be sending any money. If you’re legitimate, open escrow with a licensed title company and send a written purchase agreement.”

“Send Bitcoin to lock your price.”

You: “No legitimate real-estate transaction requires crypto from a seller. All deposits and disbursements go through a licensed title company.”

“Wire me a deposit directly so we can skip title.”

You: “I only wire to the title company listed on the purchase agreement. If you’re a real buyer, open escrow and have the title officer contact me.”

“We’re billing your card monthly for premium marketing.”

You: “I’m selling directly, not paying for marketing. Cancel any charges immediately. Do not keep my card on file.”

“We can get you a higher offer if you upgrade for $299.”

You: “Offers are based on numbers, not fees. If you have a real offer, put it in writing and open escrow with title.”

9) Already Paid or Shared Data? Do This Now.

- Call your bank/credit card to dispute charges and block recurring payments.

- Change passwords for email and financial accounts.

- Document emails, call logs, transactions, website links, and screenshots.

- If a real closing is underway, notify your title company about potential wire-fraud risk.

- Report fraud to your state Attorney General and the FTC. For wire theft, file with FBI IC3 immediately.

- Contact Local Home Buyers USA to restart your sale safely—with no fees.

Ready for a Safe, No-Fee Offer?

At Local Home Buyers USA, your protection is built into our process: no seller fees, title-first closings, transparent contracts.

10) FAQs

Should I ever pay an online property company to buy my house?

No. Legitimate home buyers pay you and close through a licensed title company or closing attorney. Upfront fees, subscriptions, or crypto requests are bright-red flags.

Is earnest money a fee I have to pay?

No. Earnest money is a buyer’s deposit held by the title company. As the seller, you do not pay earnest money to sell a house.

Can a legitimate title company ask me to wire money?

Title companies may arrange wires to you at closing (your proceeds). If you’re asked to wire out funds, confirm the purpose (payoff, taxes) and verify instructions by calling a known title-office number—not the phone number in an email thread.

Are crypto, gift cards, or P2P apps ever required in a real-estate sale?

No. Those payment methods are favored by scammers because they’re hard to reverse. Real closings route through title with bank-verified disbursements.

How fast can a legitimate buyer close?

Often in 7–21 days, depending on title work and the seller’s timeline. Speed does not require any upfront seller fees.

How do I verify a buyer is real?

Ask for a written purchase agreement, proof of funds, and the title company’s contact information. Call the title office independently to confirm escrow is open.

Sources & Notes

Figures are cited from public reports and are provided for consumer education. Always verify wire instructions with your title company via a trusted phone number.

- FBI Internet Crime Complaint Center (IC3) 2023 Report – Business Email Compromise losses. ic3.gov

- Federal Trade Commission (FTC) Consumer Sentinel Network Data Book 2023 – reported consumer fraud losses. ftc.gov

- American Land Title Association (ALTA) – wire-fraud prevention resources and industry alerts. alta.org

- FinCEN – advisories regarding real-estate wire-fraud patterns and suspicious-activity reporting. fincen.gov