How to Sell an Inherited House with Multiple Heirs

Without Letting the Estate Break the Family

A calm, step-by-step guide for multiple heirs: confirm authority, align expectations, choose a sale path, and close cleanly—while keeping relationships intact. Below, an interactive “Heir Alignment Console” turns your inputs into a friction score and next steps you can act on this week.

Educational overview only—not legal, tax, or financial advice. Always consult local professionals for your state and county.

Executive Summary: The Calmest Way to Sell with Multiple Heirs

Confirm who has legal authority (PR/executor/administrator or trustee), and what signatures the title company actually needs. Don’t start negotiations until this is clear.

Follow the probate or trust steps in order. Some counties require sale notices, overbid windows, or approvals—build these into the calendar so nobody feels blindsided.

Unresolved liens, unclear authority, or one holdout heir can stall deals. Surface blockers early and give clear, written options with deadlines.

Interactive Heir Alignment Console

Use this high-level console like a Bloomberg-style dashboard for your family’s situation. Answer a few neutral questions about heirs, paperwork, property condition, and urgency. We’ll generate a friction index, a sense of timeline pressure, and a short plan you can share on your next family call.

Contents · Your Multi-Heir Playbook

Multiple Heirs: What It Legally Means

When several people inherit a property, each person usually holds an undivided interest in the whole—nobody owns “their room.” That’s why authority and signatures matter as much as price.

Property often moves from the decedent to an estate or trust, then transfers to heirs or buyers following the will, trust, or state law plus any court orders.

If there’s a will, it typically names a personal representative (executor). Courts issue “letters” confirming their authority to act for the estate.

If there’s no will, state intestacy rules determine heirs and their priorities. The court usually appoints a personal representative to sign and manage the process.

Because states vary, verify required capacity and signatures with local counsel before listing, accepting an offer, or signing sale documents.

Probate 101: Authority, Timelines, and Documents

Probate doesn’t always mean “years of court.” But it does set the rules on who can sign, when debts must be addressed, and what the title company will require to close.

| Milestone | What It Does | Why It Matters for Sale |

|---|---|---|

| Appointment | Court appoints PR/executor/administrator. | Enables someone to sign listings, disclosures, and sale documents. |

| Letters / Authority | “Letters Testamentary/Administration” or trust certification issued. | Title/escrow typically require these to close and record. |

| Notice & Creditors | Creditors notified; claim window opens. | Debts and liens may surface; plan payoffs or reserves at closing. |

| Inventory / Valuation | Estate assets are identified and valued. | Supports pricing, tax reporting, and fair distribution among heirs. |

| Sale Approval (if needed) | Some courts require approval, notice, or overbid procedures. | Notice/overbid/confirmation can add steps and time to closing. |

| Final Accounting | PR reports activity, pays claims/fees, and distributes proceeds. | Sale proceeds get allocated to heirs according to the plan or law. |

Requirements and approvals vary by jurisdiction; consult local counsel for specifics in your county.

What “Success” Looks Like at a Glance

Keys to alignment

- Confirm authority early (PR or trustee documents in hand).

- Share the same net sheet and estimates with all heirs.

- Time-box decisions (for example 7–10 days for review and questions).

- Document agreements and circulate brief weekly updates.

Transparency turns opinions into data-driven decisions—and protects relationships while you sort out the numbers.

Aligning Heirs: Meetings, Voting, and Paper Trails

Framework: kickoff call → decision log → single point-of-contact → weekly updates. The goal is fewer surprises, fewer group texts, more clarity.

- Kickoff call: outline goals, timeline, roles, and key tasks (insurance, access, utilities, personal items).

- Decision record: short, dated log that tracks list vs. cash, repair budget, distribution basics, and key votes.

- Voting approach: majority or super-majority for non-legal choices; legal authority stays with the PR/trustee.

- SPOC: one coordinator interfaces with agents, buyers, and title; they distribute clear summaries to all heirs.

- Transparency: share net sheets, estimates, and contracts early; clarity reduces disputes and “I never saw that” moments.

Decision Trees: List vs. Cash · Repair vs. As-Is

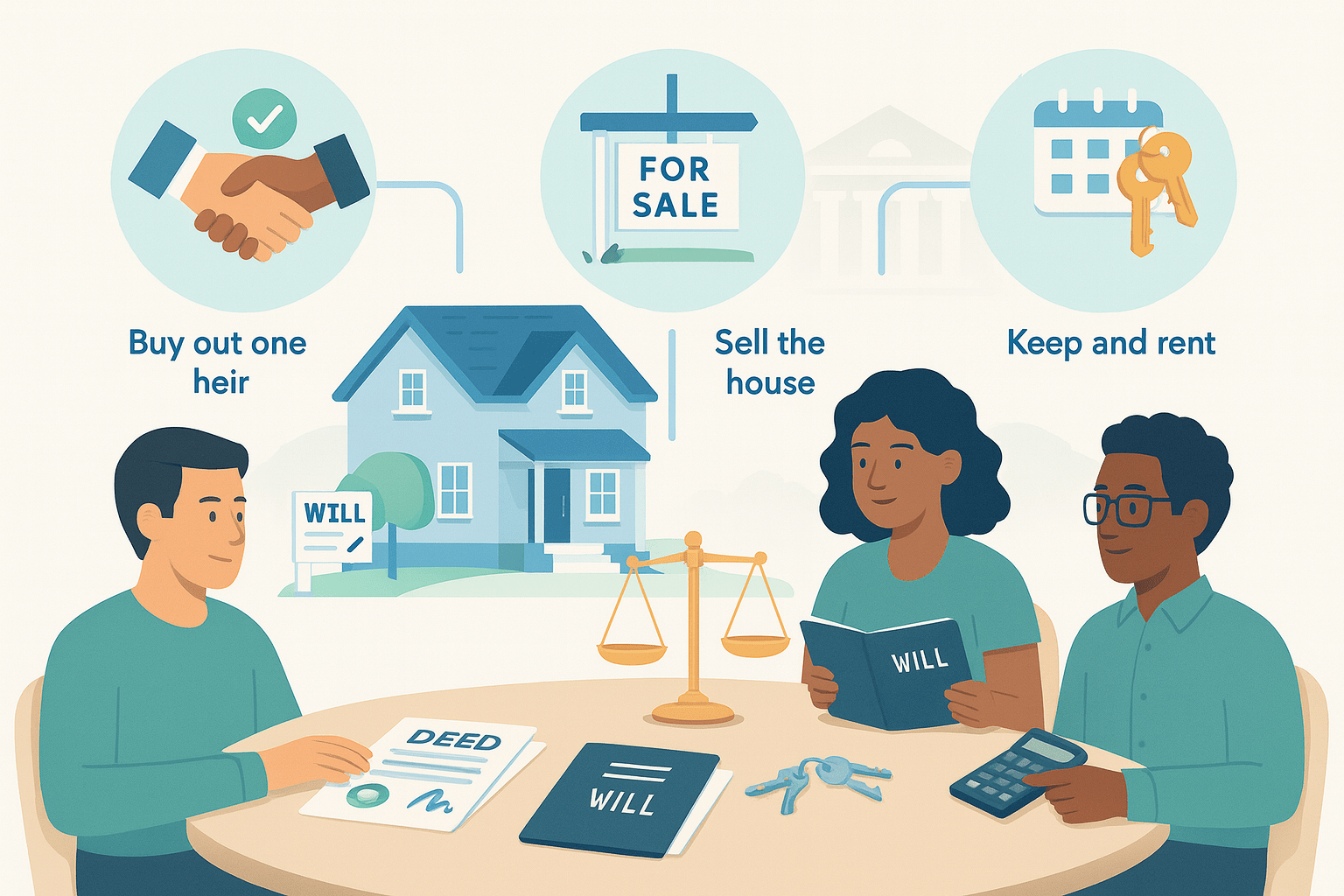

List on the Market When…

- Repairs are manageable and access is simple (no hostile tenants, minimal clutter).

- Local demand favors retail buyers, strong photos, and full marketing.

- Heirs can tolerate showings, timelines, and some inspection/appraisal risk.

Consider a Cash Offer When…

- Multiple heirs need certainty and a defined closing date they can all plan around.

- Repairs, clean-outs, or legal steps make retail timelines and buyer financing risky.

- Liens or debts require coordination and quick resolution at the closing table.

Repair vs. As-Is

- Repair if scope is limited, contractors are reliable, and the expected price lift clearly exceeds cost and time.

- Sell as-is if condition is complex, heirs are fatigued, or timelines are tight and you want to avoid re-inspection risk.

- Credits can work when underwriting allows; buyers choose materials and timing, closings stay on schedule.

Buyouts, Holdouts, and Partition Options

Buyout Basics

- Agree on a price grounded in current condition—not a perfect-world “wish list.”

- Deduct realistic selling costs and repairs where appropriate.

- Set deadlines for financing, appraisal (if any), and closing.

- Use neutral settlement and written releases to close the loop.

Addressing a Holdout

- Re-center on shared goals: fair net, calm process, and getting unstuck.

- Present structured options (for example, list for 30 days with a signed cash backup).

- Escrow small amounts for disputed items so closing can proceed while details resolve.

Partition (Last Resort)

Courts may allow partition actions, which can force a sale. Because litigation is slow and costly, families usually settle once options and deadlines are clearly presented. Always discuss with local counsel before considering this path.

Debts, Liens, HOA, and Utilities

Checklist: pull preliminary title early · request payoff letters · verify taxes/assessments · confirm HOA/COA balances · keep utilities on through appraisal/walkthrough · maintain insurance until recording.

- Mortgages & HELOCs: obtain payoffs, confirm per-diem interest and any reinstatement, late, or closing fees.

- Taxes & fines: verify property taxes, municipal fines, and assessments; some must be paid to close.

- Judgments/liens: title may need releases or court orders; start early so they don’t delay funding.

- HOA/COA: request resale certificates/estoppels and check transfer or move-in fees.

Taxes & Basis: Practical, Not Personalized Advice

Heirs often ask about capital gains and basis. Generally, the relevant valuation date helps determine basis; the sale price and allowable expenses affect gain or loss. Because tax law changes and specifics matter, speak with a qualified tax professional before distributing proceeds or filing returns.

- Document value: order an appraisal or credible market analysis tied to the appropriate valuation date.

- Track costs: keep records of allowable selling costs (commissions, title fees) and estate expenses.

- Coordinate forms: estates and heirs may receive year-end tax documents tied to proceeds and asset sales.

Informational only—this is not tax or legal advice.

Suggested Timeline & Milestones

- Weeks 0–1: confirm authority and heirs; secure the property; order preliminary title; notify insurance and utilities.

- Weeks 1–2: decide list vs. cash; gather at least two estimates for major items; share a draft net sheet with all heirs.

- Weeks 2–3: clear personal property as needed; schedule photos/showings or buyer walkthroughs.

- Weeks 3–6: accept an offer; resolve title and lien items; confirm payoffs; sign closing documents.

- Closing week: verify distribution and wiring instructions; fund and record; circulate final statements and receipts.

Vendors, courts, and lenders all set their own pace. Build buffers into the plan and communicate changes as soon as they appear.

Negotiation Scripts That De-Escalate Instead of Explode

Script A: Aligning on a Cash Offer

We have two priorities—fair net and a calm path. A cash offer with no repairs and a date-certain close gives us certainty. If a higher retail offer appears quickly, we’ll pivot; otherwise, we choose certainty to protect the family’s timeline.

Script B: Handling a Repair Dispute

Repairs would add re-inspection risk and weeks of delay. We’ll offer a credit based on two estimates so closing stays on track while the buyer chooses materials and timing.

Script C: Responding to a Low Appraisal

Let’s compare recent sales and improvements. If the gap is small, we can adjust price, share data with the appraiser, or offer a modest credit to bridge. We want the loan to fund and the closing to hold.

Script D: Addressing a Holdout Heir

Our shared goals are fair distribution and peace in the family. Two paths: (1) list for 30 days within a defined price range, then accept the cash backup; or (2) proceed with the cash offer now and reserve a small amount for your concern, released once it’s resolved.

Skip Disputes & Delays — Get a Date-Certain Cash Offer

If co-heirs want certainty, we’ll provide a no-obligation offer with a clear closing date. You see comps, a net sheet, and a path that respects the legal process and the family.